The Indy reports on Bailey of the Bank on Bitcoin, who warns, “Cryptocurrency has ‘no intrinsic value’ and investors will ‘lose all your money’, says Bank of England chief” I add, “Bitcoin only works because the ‘proof of work’ is so expensive and time consuming; and its also destructive of the environment due to its useless power consumption. (It’s also very slow, doing 700 TPS, that’s not enough for a business, let alone an economy.) …

There’s no divorce in Bitcoin

I attended a presentation hosted by the BCS, and given by Ron Ballard, based on his article in IT Now, “Blockchain: the facts and the fiction”. What he said inspired some thoughts and reminded me of others, some of which I have previously published on my blog. I wrote an article, called Learnings of Bitcoin, which was meant to be a spoof on the Borat film title and posted it on my linkedin blog, The article looks at the tight coupling of Bitcoin, and its consensus mechanism, the proof of work, together with its costs and vulnerabilities. It examines the goal of eliminating trust authorities and its questionable ability to meet the necessary roles of money as a means of exchange and a store of wealth. In the comment pushing it, I say, "This might be a bit basic for some, but you can't have a coinless immutable blockchain, at least not one based on 'proof of work'.", at which point you need to consider if there are better data storage platforms for your use case. I use more words to explore these issues below/overleaf ....

Bitcoin

This is a long diatribe at Hacker Noon about the Bitcoin bubble and the blockchain hype. I had been considering writing something similar although my focus was on the excessive use & cost of electricity to “mine” coins and the demonstrable industrialisation and economic consolidation of the mining operations.

Bitcoin, in particular, has a shrinking use as a means of exchange, as identified by this business insider preview of a Morgan Stanley opinion. This is compounded by the fact that the transaction fees are now too high for small or micro payments, and that it is not real time, (it can take minutes to clear) and thus cannot be used for transactions that require simultaneous exchange, be it a cup of coffee or a house.

The block chain does not scale well, despite the massively distributed architecture. If its performance is matched with say Visa or other significant global payment processors, VISA is rated at 60,000 transactions/sec (TPS) where as the Bitcoin maxes out at 7 TPS. So not only is it expensive, but it can’t cope with real world volume; it’s just as well that small transactions are deserting the platform.

What started me thinking this time round, was the realisation that the amount of power required to “mine” the currency grows and is now significant. While the compensation for the miners is scrip/free, the real cost in electricity and thus carbon pollution is significant. This adds to the cost, both internal but more importantly the external cost. The planet cannot afford the electricity power and the carbon footprint to virtualise global capitalism’s money supply.

Kai Stinchcombe argues that the lack of regulation is also a disincentive to use crypto currencies and examines the Etherium/DAO hack and draws the conclusion that on the whole society needs contracts to be interpreted by people, not by software.

Money must be a means of exchange, and a store of wealth, block-chain crypto-currencies are struggling and increasingly failing to be the former and it’s current price peaks , historic volatility and lack of regulator suggests it’s weak as the latter. Is it just a con? …

Digital Transformation in Europe

I attended a conference, on the Digital Transition chapter of the CoFoE final report. This was hosted by the Estonian Human Rights centre and held in Tallinn. This article contains my notes and views of what happened. The conference invited two keynote speakers but otherwise looked at the four objectives from the COFOE final report, Chapter 6 on Digitisation, which I précised on my blog [or on Medium], in working groups. The conference came to together in plenary to share its findings on the CoFoE proposals. My key takeaway may be that the Eastern European citizen’s legitimate fear of a censorious and surveillance state, will lead to a failure to regulate private sector players who are driven by profit, wealth and exploitation.

The article continues, overleaf. Please use the read more button if necessary ...

e-voting using the blockchain

I have written a couple of things about e-voting, most comprehensively in an article entitled e-voting; I was in a hurry. I came across this twitter thread which reinforces the arguments I make, although he summarises the problems as secrecy and coercion. Matthew also takes a pop at the advocates of bitcoin though and that’s because its complex, not because its private and horrendously expensive.

Why blockchains don’t solve the voting problem. Part 1/833837

Large-scale voting requires a number of complicated properties. People need to be assured that their vote will be accurately recorded and counted. But votes also have to remain secret.

— Matthew Green (@matthew_d_green) August 28, 2018

There aren’t 833837 items in the thread, or at least I haven’t found that many, I make it about 14. Why not check it out? …

Money

Money is a means of exchange and a store of wealth. Tom Walker, in his piece on Bitcoin identifies the paradox that an asset that grows in value rapidly cannot be used as means of exchange as the opportunity cost of the purchase becomes too high. This is popularised as the $1,000,000 pizza meme. …

Looking forward, looking back, fintech.

In my linkedin article on Banks & Customers, I started by talking about the workshops at Citihub’s World Conference which had posed a 10 year time horizon. Medium term horizons such as this are both liberating and challenging when considering the future of banking and business it is certain there will be massive change and since finance has been the first business to digitise, the future of ICT is a key influencer. I also received a post from Chris Skinner’s blog, “Banks face more change in the next 10 years than in the last 200”; my response on banking is encapsulated in the linkedin article, but what makes Chris’s blog article so interesting is the illustrations about how hard it is to predict the future. For instance he posts a Jetson’s style picture, created in 1966 forecasting the state of science/life in 1999. While we have some moving walkways, they are hardly ubiquitous and much of what they suggest might come to pass has not. We do not have rocket belts, city wide domes, hovering vehicles, nor flying saucers. Looking at these forecasts provoked me to look at “Blade Runner” and its inspiration, Philip K Dick’s 1968 book, “Do Androids dream of Electric Sheep?”. “Blade Runner” was made in 1982, and set in 2019, Dick wrote the story two decades earlier and set the story in 1992.

The film makes much of the existence of space flight, off world colonies and perfect humanoid (and other animal robots) which all seem to be unlikely within the next four years, but even so we are still missing the guns and flying cars but not the prevalence of rain and sushi. One of the reasons these changes are so far from the mark, is that the big bet on space travel was wrong; humanity built the internet instead. I have missed, of course, that the film is set in LA and so the rain must be symptomatic of climate change; LA Story it’s not.

Further interest around forecasting from Skinner’s article is found by his pointing at Long Bets and his selection of a number of IT predictions. Long Bets is itself a betting exchange, and some of its predictions are fairly ordinary, many are either financial or political. (I quite like the idea that exec{“helloworld”} will take a gigabyte of space and that Chelsea Clinton will become Queen of England and the USA). Skinner chooses to comment on six bets, and the score is two right, and four wrong. Netflix exists, and so does the Panoptican and that is 10 years early. We are not printing books on demand, we are streaming them, Russia is still not the world’s foremost software development centre, there is no consumer travel to the Moon, and we are some way from the prediction that there will only be three significant currencies used in the world. (US Dollar, Bitcoin and Spacemiles). However since the forecaster predicts this will occur by 2063, we have some time to go, but the dollar’s survival to 2063 would seem an evens bet today if you are a fan of Zero Hedge.

At the conference I tried to sum up, in my mind, the technical change over the last 10 years. 10 years ago having a customer portal was a big deal, distributed computing was hard and mainly in the hands of academics, and of course, the military. Google undertook its IPO in 2004, Apple launched the iPod, the most pervasive computer operating system in the world was the 32 bit Windows XP and the most current CPU chip was the Pentium M also 32 bit, although Intel/HP had launched Itanium and other RISC chip vendors had had 64 bit computing for a while. Today the most pervasive operating system/UI is Android, the most pervasive CPU architecture is ARM. The standard system architecture was shared memory, uni- or multi-processor, Compuserve/AOL was the biggest social network, today it’s gone and dwarfed by Facebook, Twitter and iTunes, consumer connection to the internet was via dialup and isdn was only just becoming available in 2004, LAN speeds have grown from 10 GBE to 100 GBE.

| 2004 | Technology | 2014 |

| CompuServe/AOL | Social Network | |

| Bespoke | Portals | Ubiquitous |

| Niche | Distributed Computing | Ubiquitous |

| Shared Memory (UMA) | System Architecture | Cloud Grid |

| Client Server | Server Collaboration Architecture | Cloud Grid |

| Windows XP | OS | Android |

| Pentium M (32 bit) | CPU | ARM |

| Storage Networks | Storage | Hadoop |

| 9.6 baud dialup | Internet Connection | 100 Mbs |

| 10 GBE | LAN Speed | 100 GBE |

| Search | Mobile Phone | |

| iPod | Apple | iPhone/iCloud/iTunes |

| Private ($54) | $350 bn ($510) | |

| $1.52 | Apple | $115 |

The last 10 years has been a story of miniaturisation, consumerisation and collaborative computing.

I.T is now much cheaper and distributed i.e. multi-system solutions are replacing the shared memory SMP systems. Software architectures are post client-server. Given this, maybe it’s right to summarise the recent history of I.T. as the evolution of Netflix and its competitors; it is a distributed network attached system using modern scale out storage and massive scale. They are exemplars in the practice and development of distributed, open-source and cloud computing and the ultimate network consumers. They at least have innovated their markets and thus brought value to their customers. They are also massively inhibited by competition from their supply chain; which is one reason they are diversifying into content creation.

When looking at the corporate landscape, as Simon Phipps observed the IT vendors are all changing up, “IBM is becoming GE, Microsoft will become IBM, Apple is becoming Microsoft, Google will become Apple”. While it depends on your views about corporate consolidation, this all leaves room at the bottom of the scale for software and social innovation. The barrier to entry for software production is relatively cheap but only if soviet style cloud or the alternative p2p models allow access to cheap IT; someone still has to pay for the chip fabs and power.

I personally think the next 10 years for IT will be about adoption not dramatic change.

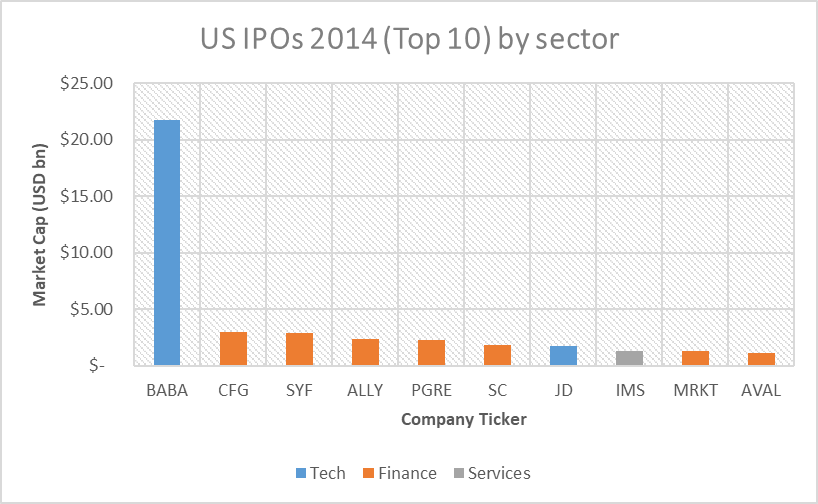

I am unclear if the IPO activity last year confirms or agrees with me. In an article published on Forbes, called Technology:Is there an IPO Boom? 2014 IPO Statistics, by Sahir Surmeli, it is shown that 7 of the top 10 US IPOs were Financial Services firms.

They were all dwarfed by Alibaba and the chart above is derived from the Forbes article. Is this further evidence that innovation is no longer in Technology?

This article was written over 2015; I didn’t publish it because I wasn’t sure it said anything useful. In 2021, I went to a seminar that asked for a 20 year forecast and it reminded me how I felt that little had changed in the 10 years up to 2014. I have backdated the article to about the date I finished it. …