My mind turns to Gardening Leave, not because I have any outstanding disputes with any of my ex-employers but because there seems to be a lack of clarity as to when and why one might use it if one was an employer.

If someone is on Gardening Leave they remain an employee and may not work for anyone else, although this also depends on the terms of the employment contract. In a world of zero hours contracts, this maybe a part of the law that will be re-examined.

For full time workers though, more and more companies are placing terms in their contracts that if one should, say, invent a new cheese in one’s back garden, then the company claims the exploitation rights. All inventions belong to your employer. It’s unclear if another month, or three months would make much difference though, but protecting the company’s intellectual property remains a motive for delaying people leaving as does getting them off site and off the IT systems.

Another key advantage is that the employee cannot work for a competitor, again, employers often via employment contracts try and restrain people’s ability to compete with them on quitting, but this is fraught with legal risk; keeping them on the books is legally much safer. Many sales staff may find themselves constrained in this way and the strengthened data protection laws will make it harder for them to take their address books with them.

A specific and unusual example of this is where staff of regulatory, political policy or law enforcement organisations leave their job to work for regulated entities. In fact, the public sector has constraints on this, but they have been weakened in time over the decades. The public sector employment contracts nearly all have clauses similar to private sector non-compete clauses but restraining public servants from working with organisations that they had regulatory or procurement relationships with. Despite this many lobbying organisations employ ex-politicians, civil servants and police. (In some ways, the movement in the other direction is more corrupt.)

The final example is where someone has financial or judicially regulated authority within the organisation. It’s usually inappropriate to leave such senior staff in place once they have resigned, and certainly of there are question marks on their remaining commitment. This of course is compounded where a compromise agreement has been signed to avoid the need to undertake disciplinary or redundancy processes. Management need to ensure that they are acting in the interests of the organisation’s stakeholders and protect themselves against a class action.

That’s where the Labour Party finds itself. A huge swath of its senior staff have put in their notice, they remain able to exercise their authority and for some reason are being permitted to work their notice, in some cases it would seem an extended notice.

It should be noted that for the ex-employee, if someone with a full time job, one or three months gardening leave can be a welcome gift. …

I recieved in my inbox an article on Adobe’s experience on abolishing their annual appraisal process. One reason was cost, they calculated it took the equivalent of 40 FTEs to run the process which illustrates the distraction of management time. The article quotes quality guru W. Edwards Deming who says,

It nourishes short-term performance, annihilates long-term planning, builds fear, demolishes teamwork, nourishes rivalry and politics.”

They replaced their previous stack ranking system with a more flexible and empowered system, divorcing formal performance from salary/bonus decisions.

It proved to be more popular with managers and staff, with one employee reporting

… that a feeling of relief has spread throughout the company because the old annual review system was “a soul-less and soul crushing exercise.”

One side effect was that involuntary terminations increased but voluntary terminations reduced, It ought to be a happier place to work. …

Simon Phipps comments on Oracle’s decision to close down the SPARC and Solaris business units. He was close to the politics of Sun’s “Dash to Open” in the mid noughties. My feeling is that Sun had failed before Schwartz was appointed; there was no longer room for differentiated hardware company; Oracle’s failure to monetise the SPARC product line may have been caused by management hubris, but the long term economics …

Over the weekend, John McDonnell promised that Income Tax would not rise for most of the country but that a higher rate would be levied on those earning more than £80,000. Tax reform can be pretty technical; and so one needs to look at one or two things without losing sight of the idea that the richer should pay their share. Each tax payer has a personal allowance of £11,500 i.e. the first £11,500 of earnings is not taxed; this is clawed back if one’s income is £100,00 or more by levying a 60% marginal rate on those earning between £100,000 and £121,200. There is probably enough room for a new additional rate between the 40% levied at £42,000 and 60% levied at £100,000 and £80,000 p.a. is a lot of money; only 3% of income earners get that much. It will remain necessary to increase the amount paid by those earning more than £145,000 and redress the regressive nature of National Insurance, which negates much of the 20% band, converting it into a 32% tax burden. Labour’s promise is also that there will be no increase in employee NICs nor in VAT, although again that’s not enough … VAT has to come down from 20%. …

I re-read Greiner’s Evolution and Revolutions as Organisations grow. He argues that the growth of companies meet crises, the resolution of which change and shape the next stage of development and that companies go through creativity, direction, delegation, co-ordination and collaboration stages. As ever, I fail to see the compulsion and inexorability of each succeeding stage but the causes of potential stagnation and the need to respond by changing the management style and tools are insightful.

I wonder where today’s exemplar corporates are on this curve, or is software different? …

The blog mirror of my storify on the #PeoplesPPE which held a conference/symposium called “The Hitchhiker’s Guide to Economics” with Yanis Varofakis, Mufti Abdur Rahman, & Anne Pettifor.

At the Real World Economics blog, Dean Baker argues that, those proposing the Reign of the Robots, have some evidence to find and that (US) economic policy makers are pursuing policies in direct contradiction to the implications of such an event. …

I went over to Hackney to attend the People’s PPE. This, their second event was called the Hitch Hiker’s Guide to Economics and I originally produced a storify, which is now here which is a collection of tweets and other social media comments about the event. The rest of this blog is based on my notes and the thoughts it provoked, on debt, banking regulation and Islamic finance, a bit less about the class war.

Ann Pettifor, Director of PRIME, opened the session, stating that the problem was debt and the banks, which create debt. …

In my linkedin article on Banks & Customers, I started by talking about the workshops at Citihub’s World Conference which had posed a 10 year time horizon. Medium term horizons such as this are both liberating and challenging when considering the future of banking and business it is certain there will be massive change and since finance has been the first business to digitise, the future of ICT is a key influencer. I also received a post from Chris Skinner’s blog, “Banks face more change in the next 10 years than in the last 200”; my response on banking is encapsulated in the linkedin article, but what makes Chris’s blog article so interesting is the illustrations about how hard it is to predict the future. For instance he posts a Jetson’s style picture, created in 1966 forecasting the state of science/life in 1999. While we have some moving walkways, they are hardly ubiquitous and much of what they suggest might come to pass has not. We do not have rocket belts, city wide domes, hovering vehicles, nor flying saucers. Looking at these forecasts provoked me to look at “Blade Runner” and its inspiration, Philip K Dick’s 1968 book, “Do Androids dream of Electric Sheep?”. “Blade Runner” was made in 1982, and set in 2019, Dick wrote the story two decades earlier and set the story in 1992.

The film makes much of the existence of space flight, off world colonies and perfect humanoid (and other animal robots) which all seem to be unlikely within the next four years, but even so we are still missing the guns and flying cars but not the prevalence of rain and sushi. One of the reasons these changes are so far from the mark, is that the big bet on space travel was wrong; humanity built the internet instead. I have missed, of course, that the film is set in LA and so the rain must be symptomatic of climate change; LA Story it’s not.

Further interest around forecasting from Skinner’s article is found by his pointing at Long Bets and his selection of a number of IT predictions. Long Bets is itself a betting exchange, and some of its predictions are fairly ordinary, many are either financial or political. (I quite like the idea that exec{“helloworld”} will take a gigabyte of space and that Chelsea Clinton will become Queen of England and the USA). Skinner chooses to comment on six bets, and the score is two right, and four wrong. Netflix exists, and so does the Panoptican and that is 10 years early. We are not printing books on demand, we are streaming them, Russia is still not the world’s foremost software development centre, there is no consumer travel to the Moon, and we are some way from the prediction that there will only be three significant currencies used in the world. (US Dollar, Bitcoin and Spacemiles). However since the forecaster predicts this will occur by 2063, we have some time to go, but the dollar’s survival to 2063 would seem an evens bet today if you are a fan of Zero Hedge.

At the conference I tried to sum up, in my mind, the technical change over the last 10 years. 10 years ago having a customer portal was a big deal, distributed computing was hard and mainly in the hands of academics, and of course, the military. Google undertook its IPO in 2004, Apple launched the iPod, the most pervasive computer operating system in the world was the 32 bit Windows XP and the most current CPU chip was the Pentium M also 32 bit, although Intel/HP had launched Itanium and other RISC chip vendors had had 64 bit computing for a while. Today the most pervasive operating system/UI is Android, the most pervasive CPU architecture is ARM. The standard system architecture was shared memory, uni- or multi-processor, Compuserve/AOL was the biggest social network, today it’s gone and dwarfed by Facebook, Twitter and iTunes, consumer connection to the internet was via dialup and isdn was only just becoming available in 2004, LAN speeds have grown from 10 GBE to 100 GBE.

2004

Technology

2014

CompuServe/AOL

Social Network

Facebook

Bespoke

Portals

Ubiquitous

Niche

Distributed Computing

Ubiquitous

Shared Memory (UMA)

System Architecture

Cloud Grid

Client Server

Server Collaboration Architecture

Cloud Grid

Windows XP

OS

Android

Pentium M (32 bit)

CPU

ARM

Storage Networks

Storage

Hadoop

9.6 baud dialup

Internet Connection

100 Mbs

10 GBE

LAN Speed

100 GBE

Search

Google

Mobile Phone

iPod

Apple

iPhone/iCloud/iTunes

Private ($54)

Google

$350 bn ($510)

$1.52

Apple

$115

Table 1: Technical Change since 2004

The last 10 years has been a story of miniaturisation, consumerisation and collaborative computing.

I.T is now much cheaper and distributed i.e. multi-system solutions are replacing the shared memory SMP systems. Software architectures are post client-server. Given this, maybe it’s right to summarise the recent history of I.T. as the evolution of Netflix and its competitors; it is a distributed network attached system using modern scale out storage and massive scale. They are exemplars in the practice and development of distributed, open-source and cloud computing and the ultimate network consumers. They at least have innovated their markets and thus brought value to their customers. They are also massively inhibited by competition from their supply chain; which is one reason they are diversifying into content creation.

When looking at the corporate landscape, as Simon Phipps observed the IT vendors are all changing up, “IBM is becoming GE, Microsoft will become IBM, Apple is becoming Microsoft, Google will become Apple”. While it depends on your views about corporate consolidation, this all leaves room at the bottom of the scale for software and social innovation. The barrier to entry for software production is relatively cheap but only if soviet style cloud or the alternative p2p models allow access to cheap IT; someone still has to pay for the chip fabs and power.

I personally think the next 10 years for IT will be about adoption not dramatic change.

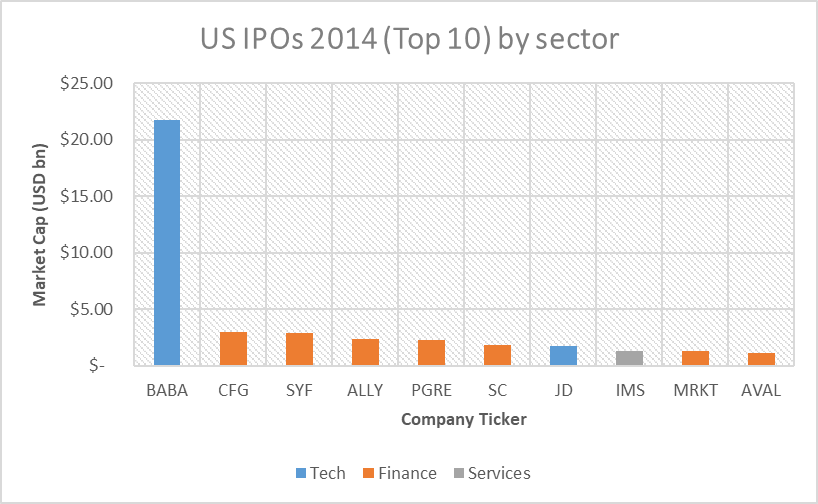

I am unclear if the IPO activity last year confirms or agrees with me. In an article published on Forbes, called Technology:Is there an IPO Boom? 2014 IPO Statistics, by Sahir Surmeli, it is shown that 7 of the top 10 US IPOs were Financial Services firms.

They were all dwarfed by Alibaba and the chart above is derived from the Forbes article. Is this further evidence that innovation is no longer in Technology?

This article was written over 2015; I didn’t publish it because I wasn’t sure it said anything useful. In 2021, I went to a seminar that asked for a 20 year forecast and it reminded me how I felt that little had changed in the 10 years up to 2014. I have backdated the article to about the date I finished it. …

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.