At the Real World Economics blog, Dean Baker argues that, those proposing the Reign of the Robots, have some evidence to find and that (US) economic policy makers are pursuing policies in direct contradiction to the implications of such an event. …

Over the last week, Google's transnational profit shielding has come into focus with HMRC agreeing that they can settle up and agreed a sweetheart deal. It's not popular, nor is it probably the most important. Amazon is probably a bigger problem for the real economy. I made a story on storify which I copied over in Jul 2020 and back dated to the date of it's original publication. See overleaf/below for the story.

I went over to Hackney to attend the People’s PPE. This, their second event was called the Hitch Hiker’s Guide to Economics and I originally produced a storify, which is now here which is a collection of tweets and other social media comments about the event. The rest of this blog is based on my notes and the thoughts it provoked, on debt, banking regulation and Islamic finance, a bit less about the class war.

Ann Pettifor, Director of PRIME, opened the session, stating that the problem was debt and the banks, which create debt. …

In my linkedin article on Banks & Customers, I started by talking about the workshops at Citihub’s World Conference which had posed a 10 year time horizon. Medium term horizons such as this are both liberating and challenging when considering the future of banking and business it is certain there will be massive change and since finance has been the first business to digitise, the future of ICT is a key influencer. I also received a post from Chris Skinner’s blog, “Banks face more change in the next 10 years than in the last 200”; my response on banking is encapsulated in the linkedin article, but what makes Chris’s blog article so interesting is the illustrations about how hard it is to predict the future. For instance he posts a Jetson’s style picture, created in 1966 forecasting the state of science/life in 1999. While we have some moving walkways, they are hardly ubiquitous and much of what they suggest might come to pass has not. We do not have rocket belts, city wide domes, hovering vehicles, nor flying saucers. Looking at these forecasts provoked me to look at “Blade Runner” and its inspiration, Philip K Dick’s 1968 book, “Do Androids dream of Electric Sheep?”. “Blade Runner” was made in 1982, and set in 2019, Dick wrote the story two decades earlier and set the story in 1992.

The film makes much of the existence of space flight, off world colonies and perfect humanoid (and other animal robots) which all seem to be unlikely within the next four years, but even so we are still missing the guns and flying cars but not the prevalence of rain and sushi. One of the reasons these changes are so far from the mark, is that the big bet on space travel was wrong; humanity built the internet instead. I have missed, of course, that the film is set in LA and so the rain must be symptomatic of climate change; LA Story it’s not.

Further interest around forecasting from Skinner’s article is found by his pointing at Long Bets and his selection of a number of IT predictions. Long Bets is itself a betting exchange, and some of its predictions are fairly ordinary, many are either financial or political. (I quite like the idea that exec{“helloworld”} will take a gigabyte of space and that Chelsea Clinton will become Queen of England and the USA). Skinner chooses to comment on six bets, and the score is two right, and four wrong. Netflix exists, and so does the Panoptican and that is 10 years early. We are not printing books on demand, we are streaming them, Russia is still not the world’s foremost software development centre, there is no consumer travel to the Moon, and we are some way from the prediction that there will only be three significant currencies used in the world. (US Dollar, Bitcoin and Spacemiles). However since the forecaster predicts this will occur by 2063, we have some time to go, but the dollar’s survival to 2063 would seem an evens bet today if you are a fan of Zero Hedge.

At the conference I tried to sum up, in my mind, the technical change over the last 10 years. 10 years ago having a customer portal was a big deal, distributed computing was hard and mainly in the hands of academics, and of course, the military. Google undertook its IPO in 2004, Apple launched the iPod, the most pervasive computer operating system in the world was the 32 bit Windows XP and the most current CPU chip was the Pentium M also 32 bit, although Intel/HP had launched Itanium and other RISC chip vendors had had 64 bit computing for a while. Today the most pervasive operating system/UI is Android, the most pervasive CPU architecture is ARM. The standard system architecture was shared memory, uni- or multi-processor, Compuserve/AOL was the biggest social network, today it’s gone and dwarfed by Facebook, Twitter and iTunes, consumer connection to the internet was via dialup and isdn was only just becoming available in 2004, LAN speeds have grown from 10 GBE to 100 GBE.

2004

Technology

2014

CompuServe/AOL

Social Network

Facebook

Bespoke

Portals

Ubiquitous

Niche

Distributed Computing

Ubiquitous

Shared Memory (UMA)

System Architecture

Cloud Grid

Client Server

Server Collaboration Architecture

Cloud Grid

Windows XP

OS

Android

Pentium M (32 bit)

CPU

ARM

Storage Networks

Storage

Hadoop

9.6 baud dialup

Internet Connection

100 Mbs

10 GBE

LAN Speed

100 GBE

Search

Google

Mobile Phone

iPod

Apple

iPhone/iCloud/iTunes

Private ($54)

Google

$350 bn ($510)

$1.52

Apple

$115

Table 1: Technical Change since 2004

The last 10 years has been a story of miniaturisation, consumerisation and collaborative computing.

I.T is now much cheaper and distributed i.e. multi-system solutions are replacing the shared memory SMP systems. Software architectures are post client-server. Given this, maybe it’s right to summarise the recent history of I.T. as the evolution of Netflix and its competitors; it is a distributed network attached system using modern scale out storage and massive scale. They are exemplars in the practice and development of distributed, open-source and cloud computing and the ultimate network consumers. They at least have innovated their markets and thus brought value to their customers. They are also massively inhibited by competition from their supply chain; which is one reason they are diversifying into content creation.

When looking at the corporate landscape, as Simon Phipps observed the IT vendors are all changing up, “IBM is becoming GE, Microsoft will become IBM, Apple is becoming Microsoft, Google will become Apple”. While it depends on your views about corporate consolidation, this all leaves room at the bottom of the scale for software and social innovation. The barrier to entry for software production is relatively cheap but only if soviet style cloud or the alternative p2p models allow access to cheap IT; someone still has to pay for the chip fabs and power.

I personally think the next 10 years for IT will be about adoption not dramatic change.

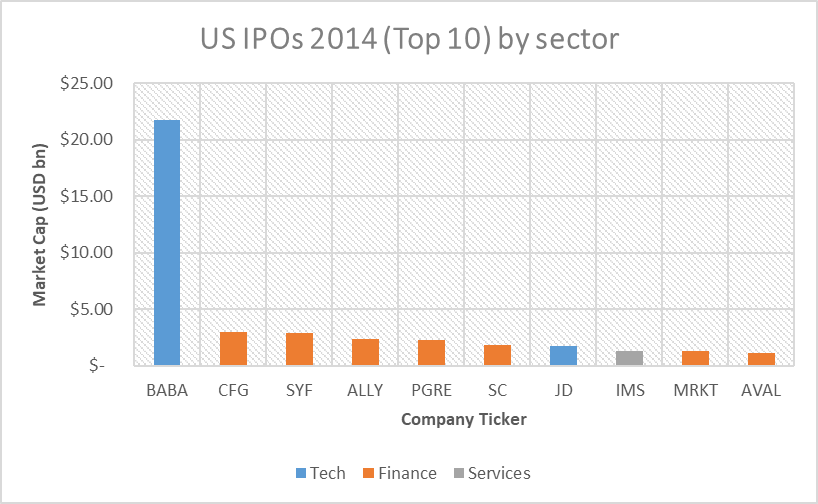

I am unclear if the IPO activity last year confirms or agrees with me. In an article published on Forbes, called Technology:Is there an IPO Boom? 2014 IPO Statistics, by Sahir Surmeli, it is shown that 7 of the top 10 US IPOs were Financial Services firms.

They were all dwarfed by Alibaba and the chart above is derived from the Forbes article. Is this further evidence that innovation is no longer in Technology?

This article was written over 2015; I didn’t publish it because I wasn’t sure it said anything useful. In 2021, I went to a seminar that asked for a 20 year forecast and it reminded me how I felt that little had changed in the 10 years up to 2014. I have backdated the article to about the date I finished it. …

How much is Capitalism changing due to the silicon revolution in the means of production. A bunch of books, articles and reviews have been released over the last few months considering the short and long term future of the techno-economy. We are on the cusp of Silicon Revolution’s “Golden Age”, when the people rein in the excesses of the capital market’s hypergrowth excesses. This story was originally created in the Summer of 2015, my hope was to read both “Post Capitalism” and “The 2nd Machine Age” and write a blog on my views as to the nature of the changes coming; but life got in the way. …

A day or two ago, Alex Little, published a blog post called ‘Lessons for Corbyn in “Lerner’s Law”’. Lerner’s law suggests that using your opponents language limits your ability to make the argument. Little quotes Bill Mitchell, the inventor of Modern Monetary Theory (MMT) as to how Labour’s leadership in articulating the Darling Plan and its successors talk about balancing the budget and fixing the deficit concede the argument to the Tories. Little’s article also points at Lerner’s economic theories, described as “functional finance” and points at the wikipedia article on it. He argues that by describing the proposed pump priming as PQE, and accepting that when growth takes off, the government may transition to bond financing, by even accepting that we need to live within our means, the theory and benefits from the a more overt radical financing will be lost. …

In the dying days of Labour’s Leadership selection, the key issues remain those of economics & strategy, but also unfortunately now one of mandate.

The debate on economics has come to be between Cooper and Corbyn. Demanding credibility is not an economic policy and so we can ignore Kendall & Burnham. I summarise the other’s two positions below and conclude that Corbyn’s economic manifesto is not just a shopping list of desirable reforms, they are a single set of reinforcing measures to fix and rebuild the economy so it works in the interests of the majority of people.

This was meant to be a short blog, emphasising the economy and virtuously circular, self reinforcing nature of Corbyn’s programme, but I also take the opportunity to look at the defence and foreign policy debate and conclude with some comments on the election process itself and Labour’s future.

I am glad I voted for Jeremy Corbyn, but I am not a Corbynista, I am Real Labour. …

Much is spoken of the sharing economy with Uber and AirBnB seen as their poster children. They’re different, Uber is an evolution of 20th century franchise business while AirBnB is an auction/liquidity service.

I have been tidying up my hard disks, and came across this paper, written by me called, “Why Monopolies make super-profits?” which I wrote in 2009/2010 to codify my thoughts on monopoly. The pseudo abstract says,

Monopolies restrict supply and offer their goods at prices above an equilibrium price, which is the opportunity cost of the resources used to make the goods. In doing so they make super-profits. This paper looks at how and why this is. It is based on an ABC of Economics, my memories of my Economics classes at school and university and a more recent reading of Begg et al’s “Economics”.

Dave LEVY

It looks at profit maximisation, supply and demand and the nature of competition. It does not look at aggregate welfare underproduction, nor on the lost social costs in building and defending the monopoly. Maybe a re-write is required. …

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.