A quick note on the budget, remembering I wasn’t as critical of last year’s as some, at least not on macro-economic grounds. I was obviously against the failure to abolish the two child cap, but also against the failure to properly fund universities, students, and local government.

So this budget is, to me, a bit meh and I agree with Fisher, why wait for a year? Still nothing on HE or Local Government finance, and the wealth taxation is very weak and poorly focused. No capital gains tax equalisation, no financial transaction tax.

The freezing of tax free allowance amounts is probably more damaging to those on the margin of the upper rate tax band but as I read it, it’s a piece of accounting magic. There were no plans to change it for the next two tax years anyway, and they can change their minds, although some of the impact will occur after the next election.

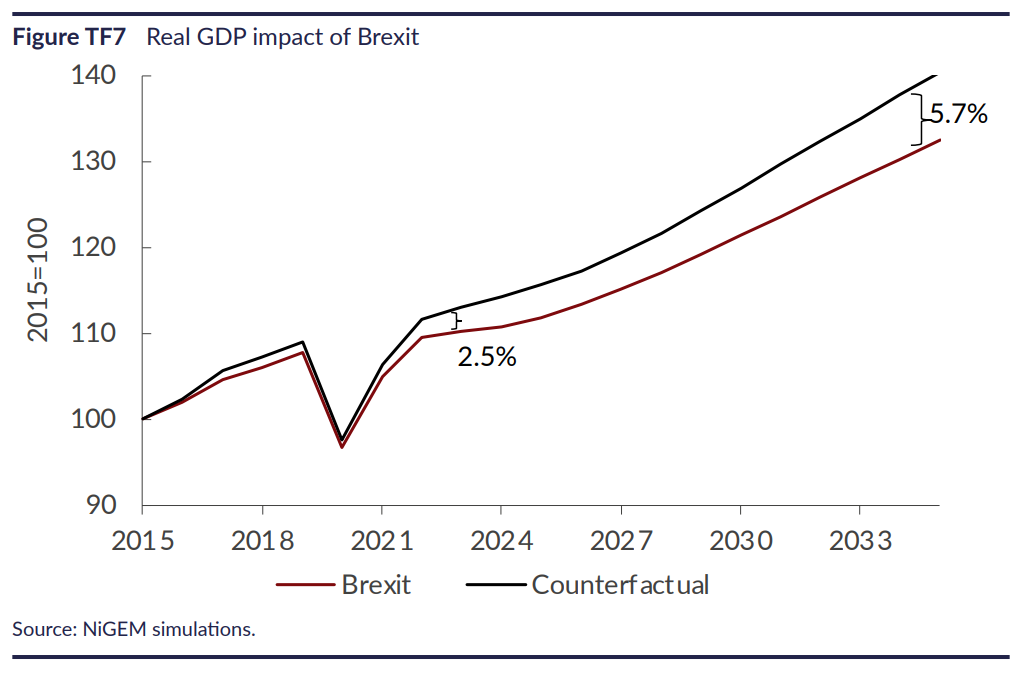

Also the FT reports that leading business people consider it insufficiently stimulating of growth, which in their case is probably not code for, “We need to rejoin the single market and customs union.”, although there are many, including me and Liz Webster, that are saying so; our macro-economic arguments recently augmented by a report from the US non-partisan National Bureau of Economic Research and by Ryan Bourne’s recanting of his pro-Brexit position.

Image Credit: from freemalaysiatoday cc 2024 by …